Recommended

Best Health Insurance for 2026

Choosing the Best Health Insurance for 2026

isn’t just about picking the cheapest...

Top 4 High-Growth Sectors.

If you are building a long-term portfolio for 2030...

7 Best Safe Stocks to Buy.

Investing in the stock market does not always mean taking high risks...

What Are ETFs and Why They

Might Be Better Than

Mutual Funds?

In recent years, the popularity of ETFs

(Exchange-Traded Funds) in India has...

INVESTING

How to Generate Regular Income from Your Investments Introduction.

How can you generate regular income from your investments? This is a common question people often ask me. Typically, we think of investments as something that will help us in old age—long-term wealth creation. But what if you want a steady income from those investments today...

INVESTING

Lenskart IPO 2025: Complete Review, Details, and Analysis Before You Invest.

Imagine if you had the chance to invest in Netflix in 2010 or Tesla in 2012. Where would you be today?

These are the kinds of opportunities that Innovation Funds aim to capture—funds that invest in today’s disruptive startups and tomorrow’s potential giant companies...

INVESTING

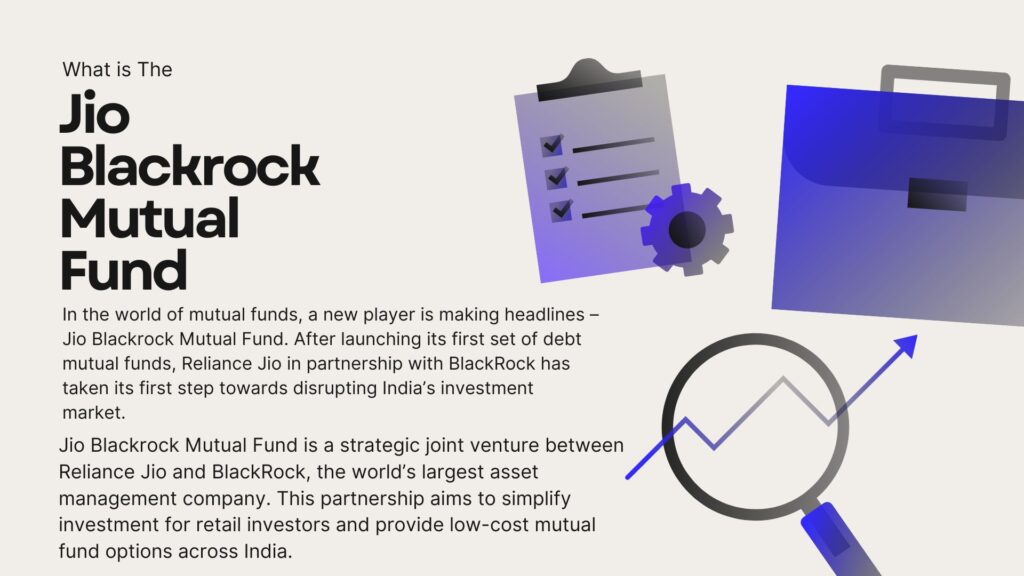

Should You Invest in Jio BlackRock Mutual Funds? A Detailed, Unbiased Review of Their New Index Funds.

Jio BlackRock has officially entered the Indian mutual fund market, and the biggest question among investors is: Should you invest in Jio BlackRock mutual funds or not? In this article, we give you a data-backed, unbiased, and clear comparison of Jio BlackRock’s index mutual funds...

STOCK MARKET

ABC of Capital Market Stocks: HDFC AMC, BSE, and CAMS Explained.

In this article, we explore the ABC of Capital Markets — three prominent stocks that represent the backbone of India’s financial ecosystem: HDFC AMC, Bombay Stock Exchange (BSE), and CAMS...

STOCK MARKET

Top 4 High-Growth Sectors for 2030 Portfolio | India Stocks.

If you are building a long-term portfolio for 2030, the focus should be on sectors with high structural growth potential. While evergreen sectors like banking, FMCG, and auto will always remain relevant, they may not deliver 25–30% CAGR returns over the next five years...

STOCK MARKET

Nykaa Share Price Analysis: Growth, Valuation & Investment Outlook.

FSN E-Commerce Ventures Ltd. — widely known by its brand name Nykaa — is a pioneer in India’s beauty, personal care, and fashion retail industry. Founded in 2012 by Falguni Nayar, Nykaa has built a strong brand identity and emerged as a leading omnichannel lifestyle retailer in India...

FINANCE

Bajaj Housing Finance Share Price: Reasons Behind the Fall and What Lies Ahead.

Imagine this — you invest in an IPO, get the allotment, and within days your stock more than doubles. Your portfolio turns green, optimism is high, and it feels like you’ve found a wealth-building machine...

STOCK MARKET

Gold vs Nifty 2025: Why Gold Has Beaten the Stock Market This Year.

TWhat’s going on with the markets? Gold is up 52% this year, while Nifty is up just 1%.

That means if you had invested ₹1 lakh in January, your gold investment would now be worth ₹1.5 lakh, while the same money in Nifty would barely be ₹1.01 lakh...

INVESTING

Lenskart IPO 2025: Complete Review, Details, and Analysis Before You Invest.

In today’s fast-paced lifestyle and continuously increasing screen time, comfortable and stylish eyewear has become essential for everyone. Meeting this demand is Lenskart, a technology-driven eyewear company that goes beyond selling glasses...

STOCK MARKET

Tata Motors Demerger: Complete Details Every Investor Should Know.

Tata Motors, one of India’s most iconic automobile giants, has announced a major corporate restructuring the Tata Motors demerger. The company is splitting its...

FINANCE

How to Generate Regular Income from Your Investments Introduction

How can you generate regular income from your investments? This is a common question people often ask me. Typically, we think of investments as something that will help us in old age—long-term wealth creation. But what if you want a steady income from those investments today?...

INVESTING

SAIL Share Price Target, Dividend History, Stock Chart, and Dividend Outlook 2025.

Steel Authority of India Limited (SAIL) is one of India’s largest and most reliable steel producers. As a Maharatna public sector undertaking (PSU) under the Ministry of Steel...

INVESTING

How to Invest in ESG: A Complete Guide for Investors.

Environmental, social and governance (ESG) has become an essential consideration for financial analysts across all industries, whether it is investment banking, commercial banking, private sector or investment management.

STOCK MARKET

Waaree Energies Share Price: Analysis, Trends, and Outlook.

In recent years, Waaree Energies share price has become a hot topic among investors tracking India’s renewable energy sector. As solar power adoption accelerates globally, companies like Waaree Energies are under the spotlight...

STOCK MARKET

Top 5 AI Stocks in India to Watch in 2025.

In today’s discussion, we will look at the top five AI (Artificial Intelligence) stocks in India. According to TeamLease Digital, the AI adoption rate in key Indian sectors such as financial services, technology, pharma, FMCG, infrastructure, and media reached around 48% in FY24...

STOCK MARKET

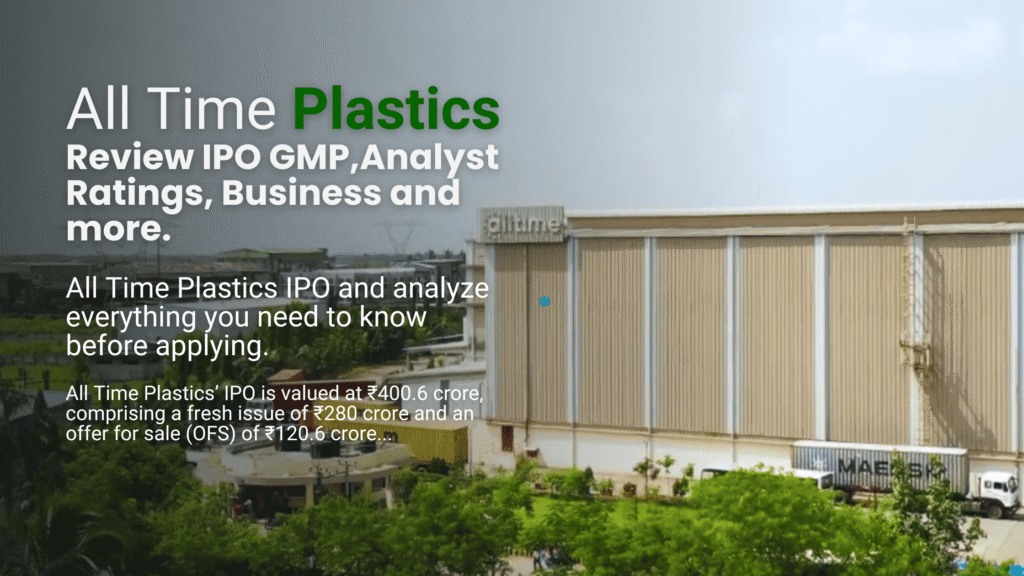

All Time Plastics IPO Review | IPO GMP, Analyst Ratings, Business and more.

Today we will be doing a detailed analysis of the IPO of All Time Plastics Ltd. - a company that manufactures plastic consumer goods. This is a company whose products you have probably seen in your kitchen, bathroom or other parts of the house ...

STOCK MARKET

How to Create BEST Mutual Fund PORTFOLIO 2025 ?

When it comes to building wealth through mutual funds, one of the most common questions investors ask is: How many mutual fund schemes should be in your portfolio? Whether you’re investing in large-cap, mid-cap, small-cap, flexi-cap, or multi-cap categories...

INVESTING

Best Mutual Funds 2025 India: A Data-Backed Guide.

If you're wondering why a "Best Mutual Funds 2025 India" video or article is still relevant when half the year has already passed, you're not alone. Many content creators rushed their videos at the beginning of the year, but the reality is—investments deserve more depth, more clarity,

STOCK MARKET

Best Mutual Funds 2025 India: A Data-Backed Guide.

If you're wondering why a "Best Mutual Funds 2025 India" video or article is still relevant when half the year has already passed, you're not alone. Many content creators rushed their videos at the beginning of the year, but the reality is...

INVESTING

Fixed Deposit vs Recurring Deposit: Which is Better for Safe Investment?

When it comes to choosing a safe investment option, most people in India compare fixed deposit vs recurring deposit. Both FD and RD are trusted by millions as they offer guaranteed returns with minimal risk. —

FINANCE

Fixed Deposit vs Recurring Deposit: Which is Better for Safe Investment?

When it comes to choosing a safe investment option, most people in India compare fixed deposit vs recurring deposit. Both FD and RD are trusted by millions as they offer guaranteed returns with minimal risk. However, choosing between these two can be confusing...

STOCK MARKET

Jio Blackrock Mutual Fund: Complete Guide, Future Plans & Investment Process.

In recent years, the popularity of ETFs (Exchange-Traded Funds) in India has surged, and for good reason. If you're looking to invest in the stock market and create long-term wealth, understanding how ETFs work can make a significant difference...

STOCK MARKET

What Are ETFs and Why They Might Be Better Than Mutual Funds?

In recent years, the popularity of ETFs (Exchange-Traded Funds) in India has surged, and for good reason. If you're looking to invest in the stock market and create long-term wealth, understanding how ETFs work can make a significant difference...

FINANCE

Top 7 Budgeting Apps in India for Smart Spending.

In a country like India where financial discipline is crucial, budgeting apps have emerged as essential tools for individuals and families to track expenses, save money, and plan for the future...

STOCK MARKET

GRSE Share Price: Latest Trends, Growth Potential & Investment Analysis.

Garden Reach Shipbuilders & Engineers Ltd (GRSE) is a leading public sector shipyard under the Ministry of Defence, primarily involved in the design and construction of...

STOCK MARKET

Premier Energies Future Plans Revealed.

Premier Energies Company was founded in April 1995. It is an integrated solar cell and solar panel manufacturing company. It is the second largest manufacturing company in the country in terms of solar cells and solar modules...

INVESTING

First IPO in the World: How the Stock Market Started.

The first IPO in the world didn’t happen in Wall Street or London—it took place in Amsterdam in the year 1602, when the Dutch East India Company (VOC) introduced a financial concept that changed global trade forever...

STOCK MARKET

What is Stock Market and How It Works.

The stock market refers to the collection of markets and exchanges where regular activities of buying, selling, and issuance of shares of publicly-held companies take place...

STOCK MARKET

5 Key Benefits of Holding Stock For Long Term.

Today we’ll talk about five benefits of holding stocks for the long term. While short-term gains can be tempting, long-term investing offers significant benefits that can lead to lasting wealth growth...